Scale Trading Strategy Across Multiple Accounts

TradeDupe

12 min read

Unlock the power of a scale trading strategy across multiple accounts. Boost your capital efficiently while managing risks. Learn how now!

A scale trading strategy for multiple accounts is the systematic replication of a single trading strategy across two or more funded accounts to amplify capital deployment without increasing per-account risk. The industry term for this practice is multi-account trade replication, and it sits at the intersection of execution technology, risk architecture, and prop firm compliance. When executed correctly, it lets you grow total position size proportionally while keeping each account's drawdown exposure within its own defined limits. Tools like Tradedupe, platforms like Tradovate, and prop firms including Apex, Topstep, and Tradeify have made this approach accessible to professional traders who treat their operation as a business rather than a series of individual bets.

What are the prerequisites and tools needed to scale trading strategies across multiple accounts?

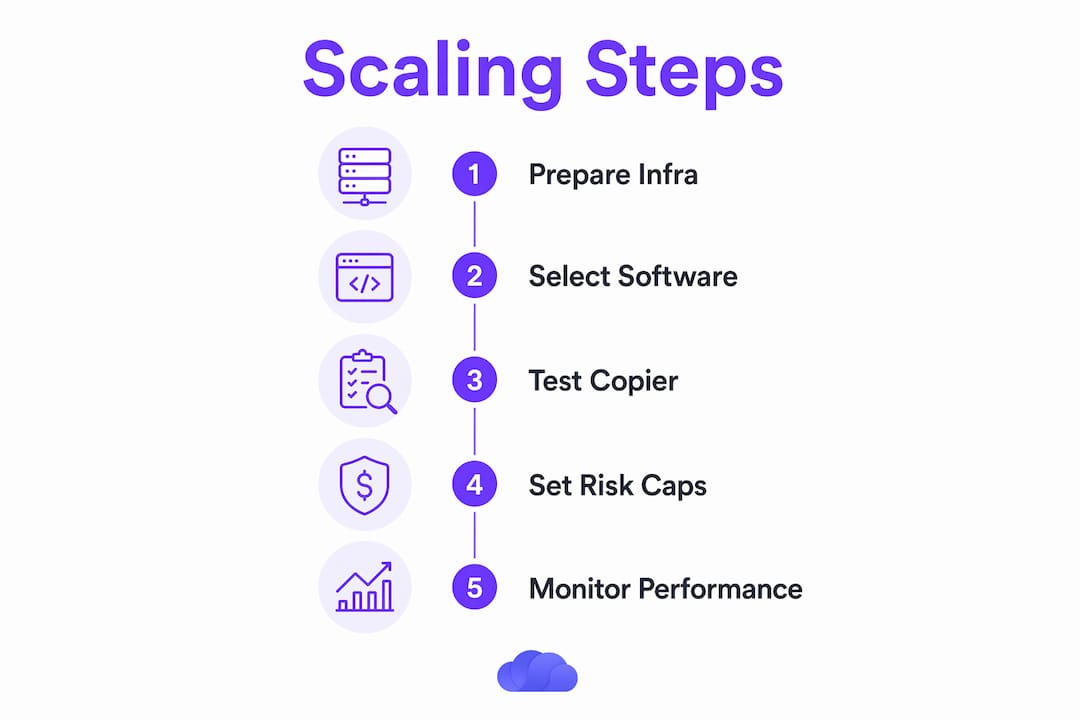

Multi-account scaling requires three layers of infrastructure before you place a single replicated trade: software, connectivity, and structural account design.

Software requirements

Trade copying software is the operational core. The best platforms synchronize not just trade entries but the complete order lifecycle, including modifications, partial fills, and cancellations. Bookmap's Multi-Account Add-on demonstrates why this matters: silent divergence between accounts builds up whenever a copier only mirrors fills and ignores subsequent order events. You need a copier that treats every order state change as a replication event. Tradedupe, for example, operates with a median execution latency of 34ms on Tradovate, which is critical for futures scalpers where a 200ms delay can mean a completely different fill price.

Key software features to evaluate:

- Synchronization modes: Orders mode (replicates the order object) vs. executions mode (replicates confirmed fills). Orders mode preserves intent; executions mode prioritizes confirmed fills.

- Risk scaling per follower: Ability to set contract multipliers or fixed lot sizes per account rather than copying the leader's raw size.

- Rogue trade detection and auto-recovery: Automatic identification of positions that deviate from the leader and forced reconciliation.

- Per-account toggle controls: The ability to pause replication on a single follower without disrupting the rest of the group.

Hardware and connectivity

A Virtual Private Server (VPS) located near your broker's matching engine reduces latency and eliminates the risk of a local internet outage breaking synchronization mid-trade. For Tradovate users, a VPS in a data center near Chicago is the standard choice. Stable, low-jitter connectivity matters more than raw bandwidth for trade copying.

| Platform | Multi-account support | Key strength |

|---|---|---|

| Tradovate | Native multi-account API | Low-latency execution, prop firm integrations |

| NinjaTrader | Third-party copier required | Advanced order types, strategy automation |

| TradingView | Webhook-based replication | Broad broker compatibility |

Pro Tip: Before scaling beyond three accounts, run your copier in simulation mode for at least five trading sessions and log every fill deviation. Rounding differences in contract sizes and symbol mapping errors surface quickly in simulation and cost nothing to fix there.

How do you implement effective risk management and exposure control when scaling multiple accounts?

The most dangerous assumption in multi-account trading is that each account operates independently. It does not. Your total market exposure is the sum of all replicated positions, and overexposure builds from execution mismatches across accounts rather than from trade quantity alone. A single ES futures contract on a $50,000 account represents a different percentage risk than the same contract on a $150,000 account. Treating them identically is the most common structural error in multi-account setups.

Building a centralized risk framework

Follow this sequence to establish exposure control before scaling:

- Define total exposure caps per symbol. Set a hard maximum number of contracts across all accounts for any single instrument. If your strategy trades ES and NQ simultaneously, cap each independently.

- Scale risk proportional to account balance, not volume. A follower account with half the balance of the leader should receive half the contract size, not an identical copy.

- Monitor execution deviations in real time. Log fill prices, timestamps, and contract sizes across all accounts after every trade. Deviations wider than one tick on liquid instruments signal a configuration problem.

- Set daily loss limits per account and aggregate. Each account needs its own stop, and you need a combined daily loss threshold that triggers a full pause across all followers.

- Review slippage reports weekly. Latency-induced fill variations compound across accounts. A 0.25-point average slippage on ten accounts is the same as a 2.5-point loss on one.

> "Overexposure in multi-account trading happens due to mismatched execution details across accounts rather than trade quantity alone." — NTK News

Pro Tip: Build a simple spreadsheet that calculates your real-time aggregate delta across all accounts. Update it after every session. When aggregate exposure approaches 80% of your total cap, reduce the leader's position size for the next trade, not after a loss.

What are the practical steps for synchronizing trades across multiple accounts?

Synchronization is where theory meets execution friction. Trade copiers can replicate trades in under 2 milliseconds, but that speed is meaningless if the configuration is wrong. Follow this setup sequence:

- Designate a single master (leader) account. This account executes all original trades. Followers never place independent orders.

- Map each follower's contract size. Use a ratio based on account balance relative to the leader. A $25,000 follower with a $50,000 leader gets a 0.5x multiplier.

- Select the correct synchronization mode. Orders mode is preferable for strategies that modify stops and targets frequently. Executions mode works for market-order-only strategies where fill confirmation is the only relevant event.

- Configure the full order lifecycle. Verify that your copier replicates entries, stop-loss adjustments, take-profit modifications, and manual exits. Precise replication demands syncing all order lifecycle events, not just fills. Failure to do so causes silent divergence.

- Run a controlled test with minimum size. Trade one contract on the leader and verify all followers receive the correct scaled size, at the expected price, within your latency threshold.

- Document manual override procedures. Define exactly how you will close all follower positions if the copier connection drops mid-trade. This procedure should take under 60 seconds.

| Synchronization mode | Best for | Risk |

|---|---|---|

| Orders mode | Strategies with active order management | Requires identical platform contexts |

| Executions mode | Market-order or automated strategies | May miss order modifications |

Handling partial fills and leverage differences

Partial fills create asymmetry across accounts. If the leader receives a partial fill of 3 out of 5 contracts, followers scaled at 0.5x should receive 1 to 2 contracts, not 2.5. Your copier must handle fractional rounding with a defined rule, either always round down to protect risk or always round to the nearest whole number for consistency. Establish this rule before live trading and document it.

Pro Tip: Test your copier's behavior on a partial fill specifically. Place a limit order in a low-liquidity session on the leader and observe how each follower handles the incomplete fill. Most configuration errors surface here, not during normal market hours.

How do prop firm rules impact scaling strategies across multiple accounts?

Most prop firms allow multiple accounts, and scaling capital across firms like Apex, Topstep, Tradeify, and Lucid Trading is a recognized approach. The operational complexity comes from the fact that each firm applies different drawdown mechanics, and a strategy that complies with one firm's rules can breach another's simultaneously.

The critical distinctions to map before scaling:

- Static drawdown: The maximum loss is calculated from the initial account balance. Once you breach it, the account is closed. This type is the most forgiving for multi-account scaling because the floor never moves.

- Trailing drawdown: The maximum loss threshold rises as your account equity rises, then locks at the high-water mark. A winning trade on one account can tighten the drawdown floor on another if both are running the same strategy with different fill prices.

- Intraday vs. end-of-day drawdown: Firms using intraday calculations penalize open unrealized losses. Firms using end-of-day calculations only count closed P&L. Damn Prop Firms recommends firms with end-of-day policies for multi-account traders because they eliminate the risk of a temporary drawdown breach during a trade that ultimately closes profitably.

> "Each prop firm has distinct drawdown rules; ignoring these differences causes breaches despite overall strategy consistency." — Damn Prop Firms

Hedging restrictions require particular attention. Some firms prohibit holding opposing positions across accounts at the same firm. Build a per-firm rules matrix that documents hedging policy, consistency requirements, daily loss caps, and third-party signal restrictions. Configure your copier to respect these boundaries at the account level, not just the strategy level.

What common challenges arise when scaling to multiple accounts?

Scaling from one account to ten does not multiply your profits linearly. It multiplies your operational surface area. Performance drift across accounts stems from rounding differences, contract specs, and latency-induced fill variations, and these discrepancies compound silently over weeks.

The most common failure points are:

- Mental load beyond five accounts: Managing ten accounts manually, even with a copier, creates cognitive overhead that degrades decision quality. Traders begin making exceptions to their rules on individual accounts, which defeats the purpose of systematic scaling.

- Unexpected drawdown breaches from rule mismatches: A trade that fits within Apex's trailing drawdown may simultaneously breach Topstep's intraday limit. Without a per-firm monitoring layer, you discover the breach after the fact.

- Behavioral traps during winning streaks: Traders often fail scaling due to abrupt risk increases. Overconfidence after a strong week leads to position size increases that violate the proportional risk framework built during setup.

- Hidden exposure drift: Rounding rules applied differently across ten accounts create a cumulative position that exceeds your intended cap. This is invisible without an aggregate exposure dashboard.

The solution is gradual scaling with hard gates. Add one account at a time. Require two weeks of clean operation before adding the next. Set a daily review practice that takes no more than 15 minutes: check aggregate P&L, review fill deviations, and confirm no accounts are within 20% of their drawdown limit. ThePropFirmGuide documents scaling phases from a few accounts to 20 or more, and the consistent finding is that traders who scale gradually maintain compliance rates far above those who add accounts in batches.

Key takeaways

Scaling a trading strategy across multiple accounts succeeds when risk is managed at the aggregate level, synchronization covers the full order lifecycle, and each prop firm's rules are mapped and enforced independently.

| Point | Details |

|---|---|

| Aggregate exposure is the real risk unit | Set hard caps per symbol across all accounts, not just per account. |

| Full lifecycle sync prevents drift | Replicate entries, modifications, cancellations, and exits, not fills alone. |

| Prop firm rules require a per-firm matrix | Map drawdown type, hedging policy, and daily loss caps for each firm separately. |

| Gradual scaling outperforms batch expansion | Add one account at a time with a two-week clean-operation gate before the next. |

| Execution speed matters for futures | Trade copiers operating under 2ms latency are the baseline for scalping setups. |

Why most traders scale wrong before they scale right

I have watched traders build technically sound multi-account setups and still blow accounts within 60 days. The failure is almost never the copier. It is the assumption that adding accounts is the same as adding capital. It is not. Adding accounts adds operational complexity, compliance surface area, and psychological pressure. The traders who scale successfully treat the operation like a business with documented processes, not a trading desk with more screens.

The most underrated decision in multi-account scaling is copier selection. Most traders evaluate copiers on latency alone. Latency matters, but the more important feature is how the copier handles exceptions: partial fills, connection drops, mismatched contract sizes, and rogue positions. A copier that handles the normal case well but fails on edge cases will cost you more in a single incident than a year of subscription fees.

City Traders Imperium's research points to a behavioral shift worth acknowledging: many traders now use multi-account setups to increase evaluation pass probability rather than to compound consistent performance. That approach treats scaling as a lottery strategy rather than a business strategy. It works until it does not, and when it fails, it fails across all accounts simultaneously.

Start with two accounts. Run them for a month. Review every fill deviation, every compliance flag, and every moment where you considered making an exception to your rules. If that month is clean, add a third. Decade-long consistency in this business comes from systems that survive bad weeks, not from setups that maximize good ones.

> — Andres

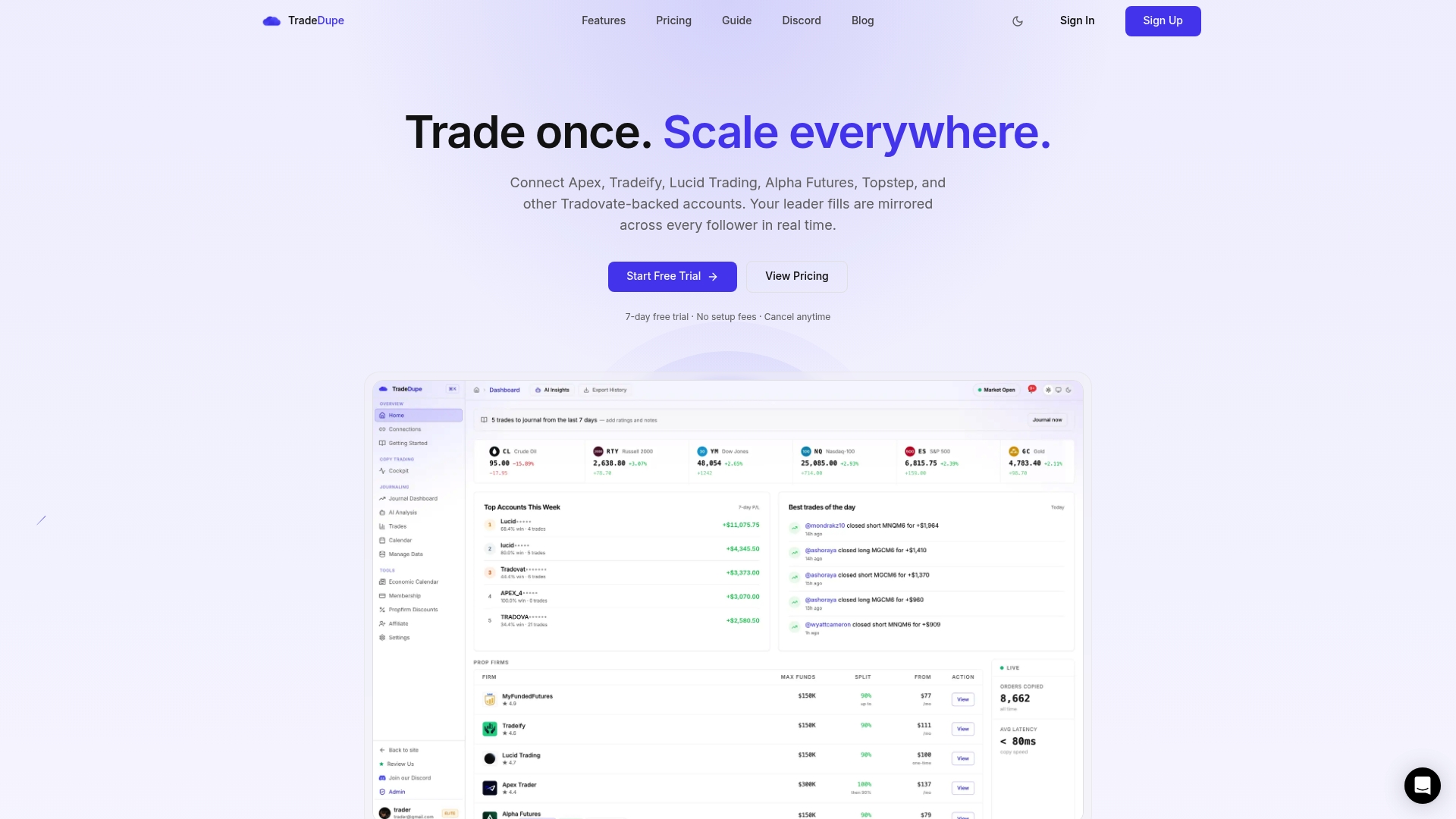

How Tradedupe simplifies scaling your trading strategy across multiple funded accounts

Tradedupe is built specifically for prop traders scaling across multiple Tradovate accounts, with direct integrations for Apex, Topstep, Tradeify, Lucid Trading, and Alpha Futures.

The platform replicates trades with a median latency of 34ms, supports both Orders and Executions synchronization modes, and provides per-account risk controls including auto-liquidation and rogue-trade detection. The centralized dashboard gives you real-time visibility into sync status, aggregate exposure, and per-account P&L without switching between platforms. Whether you are managing three accounts or thirty, Tradedupe's multi-account platform handles the operational layer so you can focus on the strategy. You can also explore the trade copier software guide to understand exactly how replication works before committing to a setup. Get started in under 10 minutes with the step-by-step onboarding guide.

FAQ

What is a scale trading strategy for multiple accounts?

A scale trading strategy for multiple accounts is the systematic replication of one trading strategy across two or more funded accounts using trade copying software, with risk sized proportionally to each account's balance rather than copied at identical volume.

How many prop firm accounts can you trade simultaneously?

Most prop firms allow multiple accounts, and experienced traders commonly operate between five and twenty accounts across different firms. The practical limit is determined by your copier's capacity and your ability to monitor compliance rules per firm.

What is the difference between orders mode and executions mode in trade copying?

Orders mode replicates the order object itself, including all modifications and cancellations, making it ideal for strategies with active order management. Executions mode replicates only confirmed fills, which suits fully automated or market-order-only strategies.

How do I avoid overexposure when trading across multiple accounts?

Set fixed total exposure caps per symbol across all accounts and use a copier that enforces risk boundaries dynamically. Overexposure builds from execution mismatches, not trade quantity, so monitoring aggregate delta after every session is the core control mechanism.

Can I use the same strategy across prop firms with different drawdown rules?

Yes, but you must configure your copier and position sizing independently for each firm's drawdown type. Firms using trailing drawdown require tighter per-account risk limits than those using static or end-of-day drawdown calculations.